Global economic forces continue to roil as financial uncertainties persist – not only those relating to European sovereign debt crises, but also our own on-shore concerns. Thus a Q3 that logs in as the worst quarter since 2009 for the Dow Jones – this sobering fact coupled with a 160% increase in the “volatility index” (VIX).

But that just tells us about equity markets. By contrast (and comparing Q3 2010 real estate data with Q3 2011 data), available figures paint a substantially different picture for San Francisco real estate. A few examples:

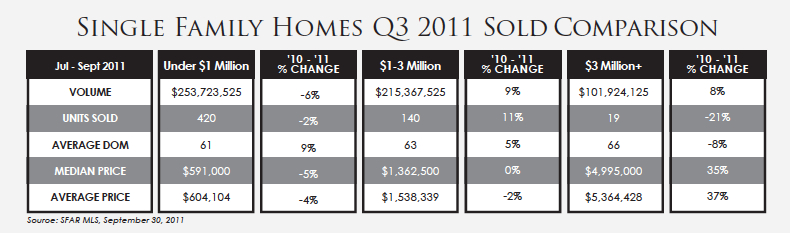

– Single family homes (SFHs) above $3M showed 35% and 37% increases in median and average sales prices (respectively) and an overall dollar sales volume up 8% from Q3 2010.

– SFHs $1M to $3M saw negligible change as to median and average prices (0% and -2%), with sales volume improving by a generous 9%.

– SFHs under $1M registered a mere 4-5% drop in median and average prices; sales volume was lower by a modest 6%.

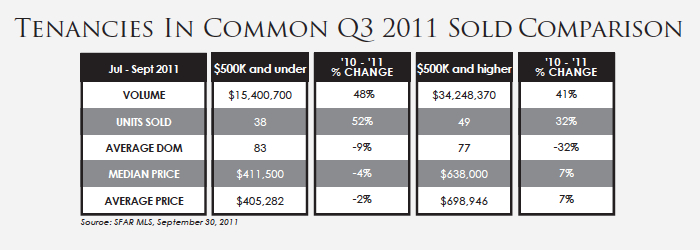

– Condos over $2M saw a 4% drop in average sales price, with sales volume off by the same figure (note: condo statistics exclude new condo sales not reported to MLS).

– Condos $1M to $2M experienced a 10% drop in overall sales volume, but median and average sales prices remained virtually unchanged.

– Condos under $1M showed a solid, and essentially unchanged, sales volume, with median and average prices steady at a modest -1% and -2%.

Armed as they are with plenty of meaningful comparable sales data and evidence of the consequences of over-priced listings, Sellers have acquired an increasingly realistic view of the marketplace. Wise Sellers have recognized that elevated “days on market” numbers are not a Seller’s friend and don’t get the property sold. MLS statistics confirm that homes on the market for over 90 days sold on average at 89% of original list price, while homes that moved within 30 days of being placed on the MLS sold at nearly 90% of original list price.

“Precision pricing” in this market is demonstrably paramount in achieving not only a timely sale but also maximizing Seller proceeds.

For their part, Buyers have become increasingly educated on and conversant with recent transactional trends, including new inventory (which, by the way, is substantially below 2010 YTD figures) and recent sales. We find Buyers to be generally patient, focused, value-sensitive and, ultimately, unwilling to make offers on overpriced listings – which is to say qualified Buyers concentrate on the best-priced inventory. They approach the primary home market in terms of investing in a home vs. speculating on an appreciating housing market.

For our part, we occasionally entertain ourselves by observing how the past three years have resembled a series of Groundhog Days: however volatile national and international news reports seem to be, we still wake up in the morning to see significant Buyer and Seller opportunities in our markets on a daily basis.

Real estate is a very local business – we have micro-markets within San Francisco (and surrounding communities) that are robust, others being less so. We welcome the opportunity to visit with you about your specific housing interests and needs and about the real estate market in general.

Click to enlarge.